Slum Upgrading and Housing Finance Framing the Debate

The document “Slum Upgrading and Housing Finance” explores the intricate relationship between slum upgrading initiatives and housing finance mechanisms. It emphasizes the necessity for innovative financial solutions to improve living conditions in slums, which are home to millions globally. The report outlines key challenges, successful strategies, and recommendations for enhancing access to housing finance for low-income populations.

Further reading:

[PDF] Low Income Shelter Finance in Slum Upgrading | Urban Institute urban

[PDF] Slum Upgrading and Housing Finance – Habitat for Humanity habitat

Context of Slum Upgrading

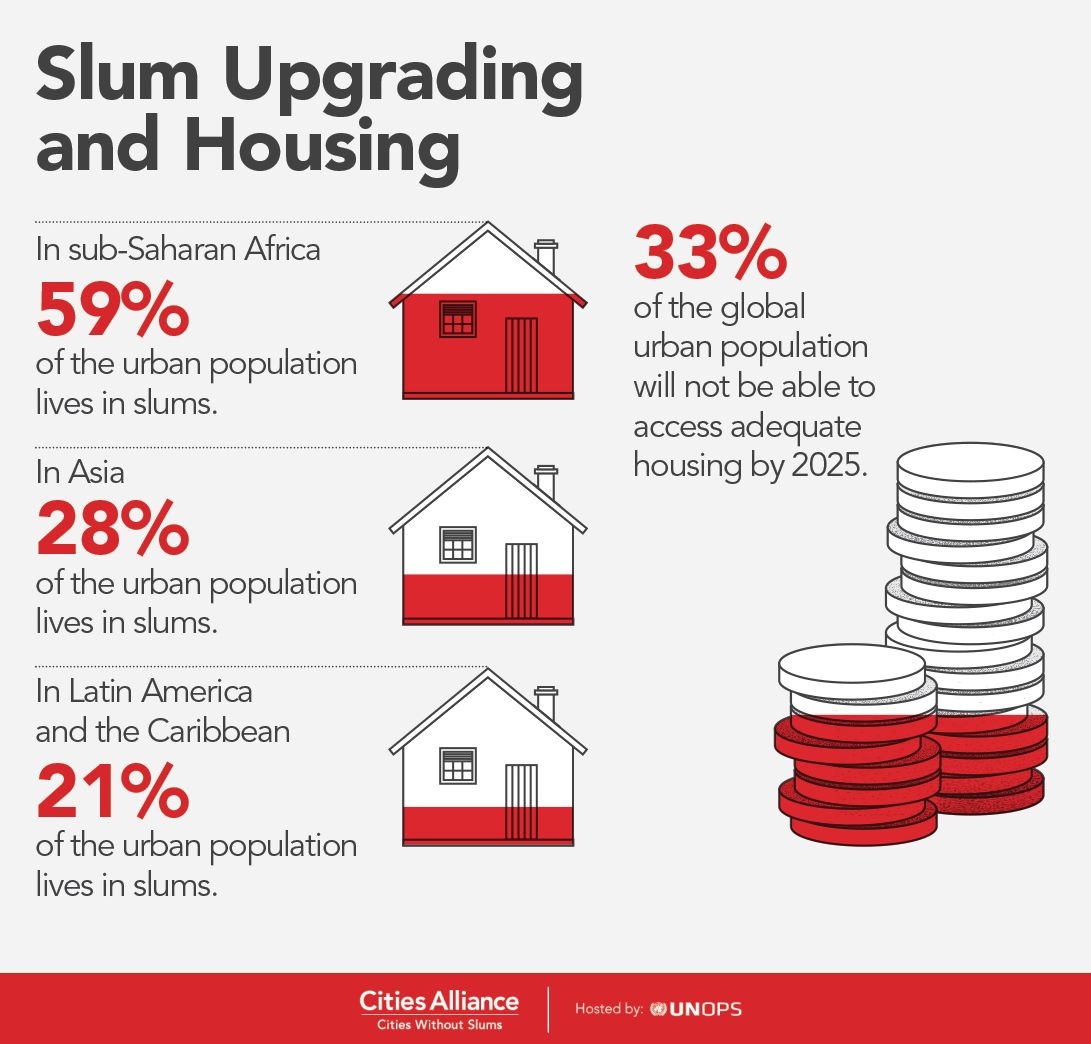

The rapid urbanization witnessed in many developing countries has led to a significant increase in slum populations. An estimated one billion people live in slums, facing inadequate housing, lack of basic services, and insecure land tenure. This situation necessitates effective slum upgrading strategies that not only improve physical infrastructure but also enhance residents’ economic opportunities.

Challenges in Housing Finance

A major barrier to successful slum upgrading is the lack of affordable housing finance. Traditional mortgage systems often do not cater to the needs of low-income households, primarily due to:

- Affordability Issues: Many low-income families cannot meet the debt service requirements associated with conventional loans. The gap between income levels and mortgage affordability is substantial.

- Inadequate Legal Framework: Most low-income households lack formal land titles, making it challenging to secure loans against their properties.

- Risk Aversion from Financial Institutions: Banks and financial institutions often perceive lending to slum dwellers as high-risk due to their informal income sources and unstable living conditions.

Successful Strategies for Financing

Despite these challenges, several innovative financing models have emerged that show promise in facilitating slum upgrading:

- Microfinance: Microfinance institutions (MFIs) have begun to provide small loans tailored for housing improvements. These loans help families incrementally upgrade their homes without the burden of large debt.

- Community Savings Groups: Initiatives that encourage community savings can empower residents to pool resources for housing improvements. This model fosters local ownership and accountability while reducing reliance on external funding.

- Public-Private Partnerships (PPPs): Collaborations between government entities and private developers can leverage resources for large-scale slum upgrading projects. These partnerships can help mobilize both public funds and private investment.

- Subsidy Programs: Government subsidies can bridge the affordability gap for low-income households, making housing finance more accessible. These subsidies can be structured to complement microfinance efforts, enhancing overall impact.

Case Studies and Examples

The report highlights various successful case studies from around the world:

- Ahmedabad’s Slum Networking Project: This initiative integrates basic services into slum areas while promoting community participation in planning and implementation.

- Nairobi’s Muungano Alliance: This community-led approach emphasizes savings and loan schemes that allow residents to finance their own housing improvements while ensuring no one is permanently displaced during upgrades.

- Nagpur’s Housing Finance Model: Combining microfinance with government subsidies has shown potential in improving housing conditions for slum dwellers by making financing more affordable.

Recommendations for Policy Makers

To effectively address the challenges of slum upgrading and housing finance, the document recommends several actions:

- Develop Inclusive Financial Products: Financial institutions should create products specifically designed for low-income households that consider their unique income patterns and repayment capacities.

- Strengthen Legal Frameworks: Governments should work towards formalizing land tenure systems to enhance security for slum residents, facilitating access to credit.

- Enhance Capacity Building: Training programs for local authorities and financial institutions can improve understanding of the needs of low-income communities, leading to better-targeted financial solutions.

- Promote Stakeholder Collaboration: Encouraging partnerships among government agencies, NGOs, financial institutions, and community organizations can lead to more comprehensive and sustainable upgrading strategies.

Conclusion

The interplay between slum upgrading initiatives and housing finance is critical in addressing urban poverty. By adopting innovative financing mechanisms and fostering community participation, stakeholders can significantly improve living conditions in slums worldwide. The document underscores that with appropriate support and resources, slum dwellers can contribute substantially to their upgrading processes, leading to more resilient urban communities.